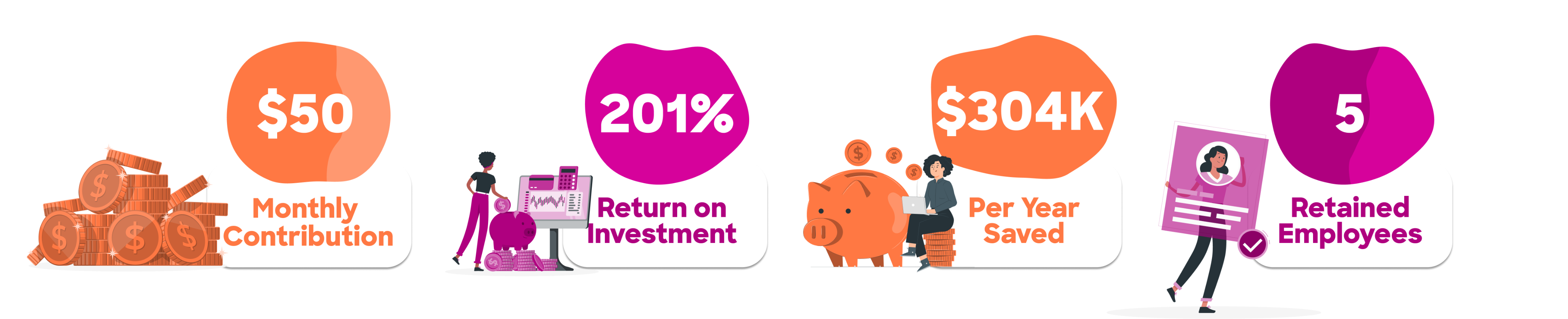

Hire and retain employees by offering Vault Pay, Vault 529, Vault Match, and Vault Tuition Reimbursement benefits. Vault helps employers contribute secure, easy-to-track student loan contributions, 529 contributions, and tuition benefits to your employees. Fully-customizable plans and on-demand employer dashboards let employers track the real-time benefits of each program.